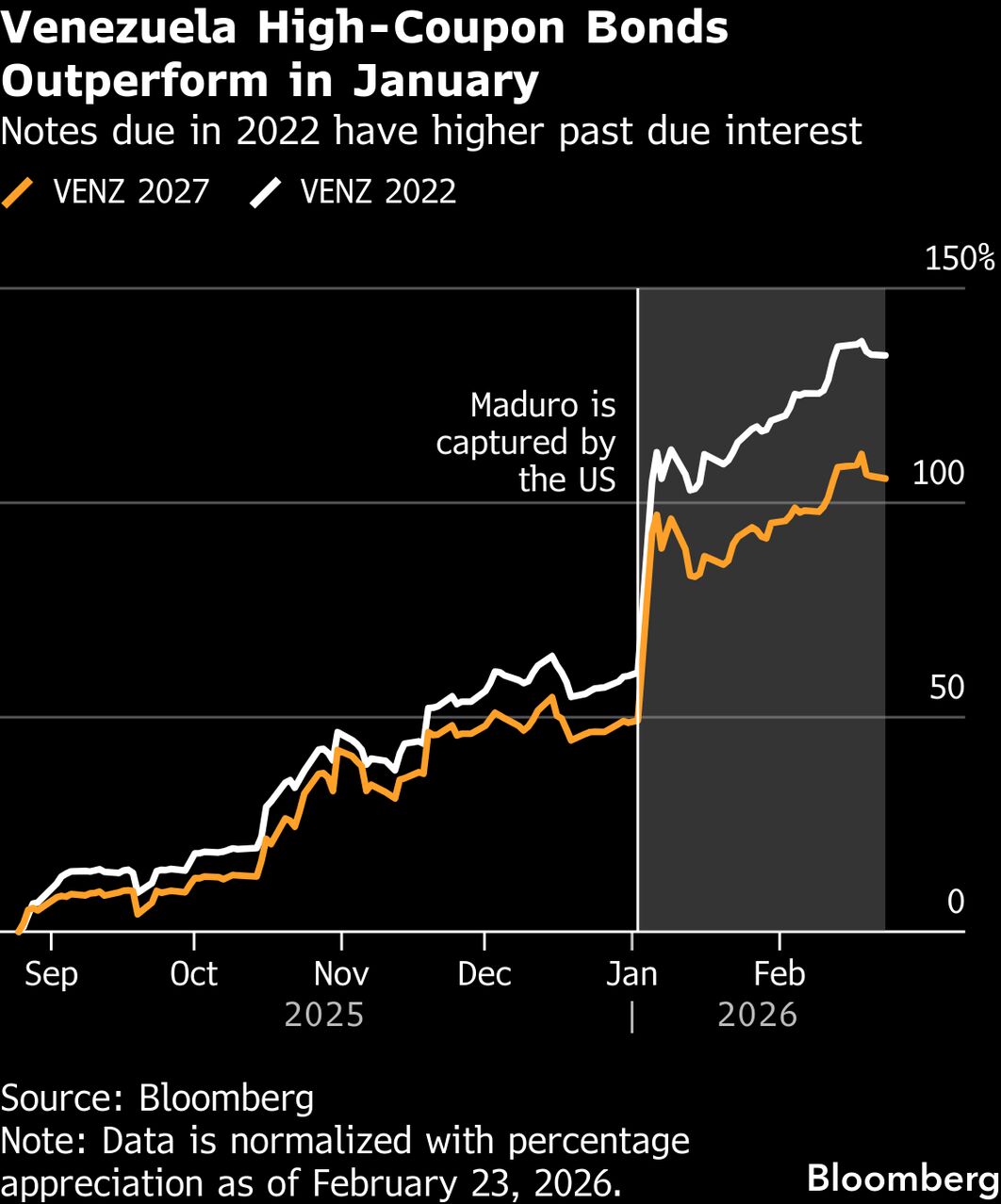

Venezuela’s Debt Revival: A Canary in the Coal Mine for Emerging Market Risk?

Over $60 billion in defaulted debt. That’s the staggering figure hanging over Venezuela, and now, surprisingly, JPMorgan and Bank of America are suggesting investors consider a gamble on Venezuelan bonds. But this isn’t about a sudden economic turnaround; it’s a calculated bet on accrued interest, a complex dance with ‘vulture funds,’ and a potential harbinger of a broader shift in emerging market risk assessment. **Venezuelan bonds** are attracting attention, but the reasons are far more nuanced – and potentially troubling – than a simple recovery story.

The Allure of Accrued Interest: A Distressed Debt Play

The recent recommendations from JPMorgan and BofA aren’t based on faith in Venezuela’s economic stability. Instead, they hinge on the massive accumulation of unpaid interest on the country’s defaulted bonds. As Bloomberg reports, these bonds offer potentially high returns if Venezuela were to eventually restructure its debt and begin making payments. This makes them attractive to investors specializing in distressed debt – those willing to take on significant risk for the possibility of substantial gains.

Navigating the ‘Vulture Fund’ Landscape

However, the path to recovery is fraught with challenges. The Venezuelan debt saga has already attracted the attention of ‘vulture funds’ – investment firms that purchase debt at deeply discounted prices and aggressively pursue full repayment, often through legal action. As El Nacional points out, these funds can complicate any potential restructuring process, demanding maximum returns and potentially hindering a broader agreement with creditors. The presence of these actors adds a layer of uncertainty and could significantly impact the ultimate value recovered by investors.

Beyond Venezuela: A Broader Trend in Emerging Market Debt?

The interest in Venezuelan bonds isn’t an isolated event. It reflects a growing appetite for risk in emerging markets, fueled by a search for yield in a low-interest-rate environment. But it also signals a potential shift in how investors are evaluating sovereign debt. Traditionally, economic fundamentals were paramount. Now, the focus is increasingly on the potential for legal recovery, even in cases where the underlying economy remains deeply troubled.

The Oxford Economics Cautionary Note

Oxford Economics offers a crucial counterpoint, warning of a “high risk of disappointment” despite the potential for short-term gains. Bloomberg Linea highlights this skepticism, emphasizing that political instability and a lack of meaningful economic reform continue to plague Venezuela. This divergence in opinion underscores the inherent volatility of investing in distressed sovereign debt. The potential for political upheaval, changes in government policy, or further economic deterioration could quickly wipe out any gains.

The Future of Distressed Sovereign Debt: A New Normal?

The Venezuelan case could set a precedent for how distressed sovereign debt is approached in the future. If investors are successful in recovering a portion of their investment, it could encourage similar strategies in other countries facing debt crises. This could lead to a surge in activity from vulture funds and a more aggressive approach to debt recovery. However, it also carries the risk of exacerbating debt problems and hindering economic recovery in vulnerable nations.

The increasing willingness to bet on accrued interest, even in the face of significant economic and political risks, suggests a growing tolerance for complexity and a willingness to accept higher levels of uncertainty. This trend could have far-reaching implications for the global financial system, potentially creating new vulnerabilities and increasing the risk of future debt crises.

| Metric | Venezuela (2024) | Global Emerging Market Average |

|---|---|---|

| Total Debt (USD Billions) | $60+ (Defaulted) | $4,000+ |

| Default Rate | 100% | 3-5% |

| Potential Return (Distressed Debt) | 20-50%+ (Highly Speculative) | 5-15% |

The situation in Venezuela is a complex interplay of financial speculation, legal maneuvering, and political realities. It’s a stark reminder that investing in emerging markets requires a deep understanding of both economic fundamentals and the potential for unforeseen risks. The coming months will be crucial in determining whether the current interest in Venezuelan bonds is a sign of a genuine recovery or simply a temporary bubble fueled by opportunistic investors.

Frequently Asked Questions About Venezuelan Bonds

What is the biggest risk associated with investing in Venezuelan bonds right now?

The biggest risk is political instability and the potential for further economic deterioration in Venezuela. Even with accrued interest, a change in government or a worsening economic situation could lead to a complete loss of investment.

Are ‘vulture funds’ a positive or negative force in the Venezuelan debt situation?

Vulture funds are a double-edged sword. They can provide liquidity to distressed debt markets, but their aggressive pursuit of full repayment can also complicate restructuring efforts and hinder a broader agreement with creditors.

Could the Venezuelan debt situation impact other emerging markets?

Yes, the outcome of the Venezuelan debt situation could set a precedent for how distressed sovereign debt is approached in other countries. A successful recovery could encourage similar strategies, while a failure could deter investors and exacerbate debt problems elsewhere.

What should investors do before considering Venezuelan bonds?

Investors should conduct thorough due diligence, understand the significant risks involved, and consult with a financial advisor. This is a highly speculative investment and is not suitable for all investors.

What are your predictions for the future of distressed sovereign debt? Share your insights in the comments below!

Keep reading

Discover more from Archyworldys

Subscribe to get the latest posts sent to your email.