Employer-Sponsored Weight Loss Drug Coverage Faces Scrutiny Amid Rising Costs

A growing number of large companies are offering coverage for GLP-1 receptor agonists – a class of drugs initially developed for diabetes but increasingly used for weight loss – but concerns about the substantial financial implications are prompting some employers to reconsider their benefits plans. The rising cost of these medications is leading to potential adjustments in coverage policies, impacting access for employees seeking these treatments.

The Rising Tide of GLP-1 Drug Coverage in the Workplace

For years, employer-provided health insurance has been a cornerstone of American healthcare. Now, that system is facing a new challenge: the increasing demand – and cost – of GLP-1 receptor agonists like semaglutide and liraglutide. These drugs, marketed under names like Ozempic and Wegovy, have demonstrated significant efficacy in promoting weight loss, leading to a surge in prescriptions.

Initially, many employers followed standard protocols, covering these medications primarily for individuals with diagnosed diabetes. However, as off-label use for weight loss became more prevalent, and as the drugs gained widespread attention, pressure mounted to extend coverage to a broader employee base. Many companies responded, recognizing the potential health benefits associated with weight loss, such as reduced risk of heart disease and type 2 diabetes.

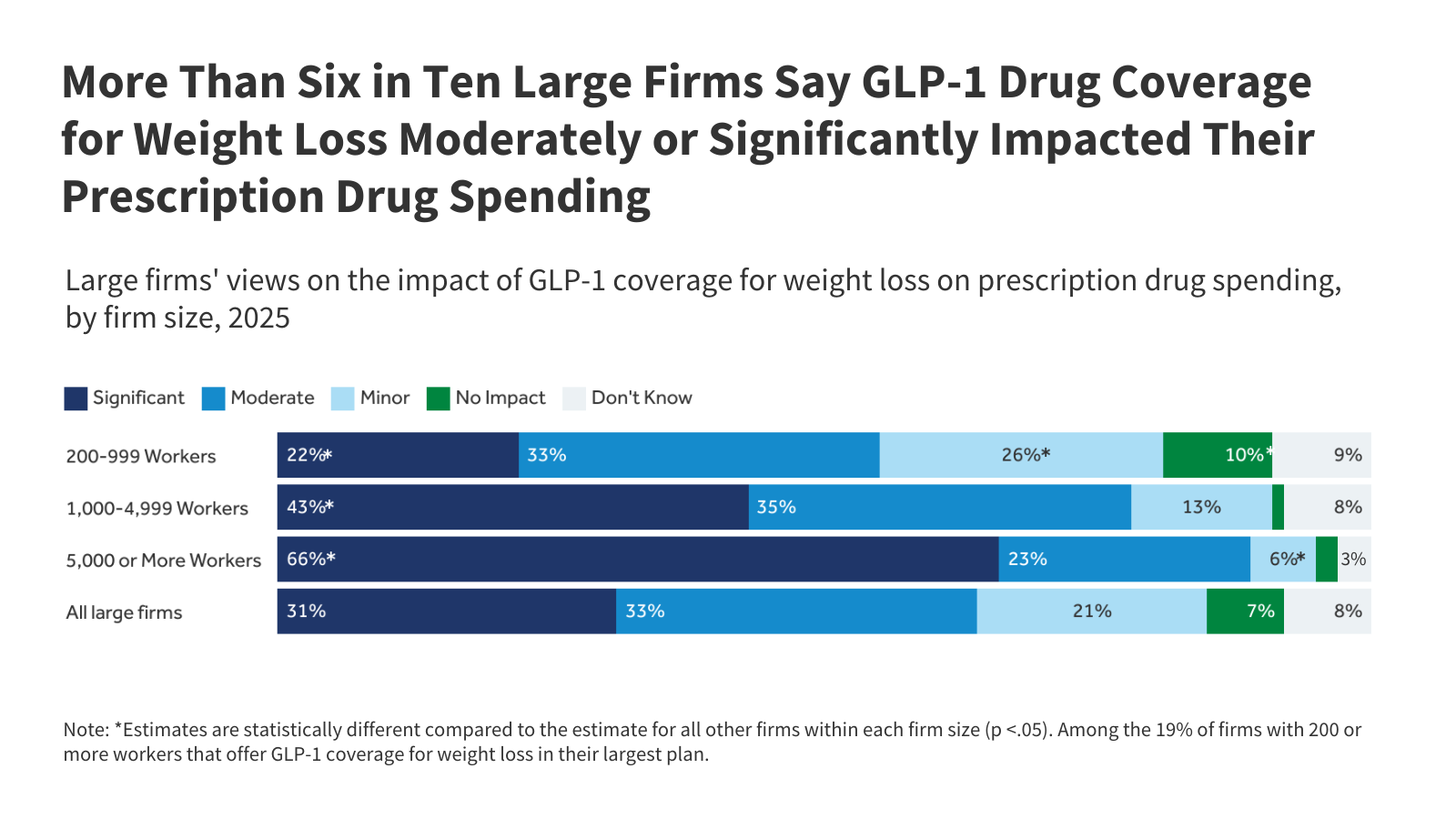

Cost Concerns Drive Policy Re-evaluation

Despite the potential benefits, the high price tag of GLP-1 drugs is causing significant budgetary strain. A single monthly prescription can easily exceed $1,300, creating a substantial financial burden for both employers and employees. This has led many organizations to explore ways to manage costs, including implementing stricter eligibility criteria, requiring prior authorization, or increasing cost-sharing for employees.

Recent conversations with benefits managers, as reported by the Kaiser Family Foundation (KFF), reveal a growing trend of employers considering scaling back coverage. Some are adding or strengthening existing requirements, such as mandating a certain Body Mass Index (BMI) or requiring participation in a weight management program before coverage is approved. Others are exploring alternative approaches, like covering the drugs only for a limited duration or focusing on preventative care initiatives.

The situation raises a critical question: how can employers balance the desire to provide comprehensive healthcare benefits with the need to control costs and maintain financial sustainability? Is it possible to create a system that ensures equitable access to these potentially life-changing medications while also protecting the financial health of both employers and employees?

Furthermore, the long-term effects of GLP-1 drugs are still being studied. While initial results are promising, more research is needed to fully understand the potential risks and benefits. This uncertainty adds another layer of complexity to the decision-making process for employers.

To gain a broader perspective on the evolving landscape of healthcare benefits, consider exploring resources from the Society for Human Resource Management (SHRM). They offer valuable insights into the challenges and opportunities facing employers in today’s dynamic healthcare environment.

Frequently Asked Questions About GLP-1 Drug Coverage

-

What are GLP-1 drugs and why are they gaining popularity?

GLP-1 receptor agonists are a class of medications originally designed to treat type 2 diabetes. They work by mimicking the effects of a natural hormone that regulates blood sugar and appetite, leading to weight loss as a side effect. Their effectiveness in promoting weight loss has driven their increasing popularity.

-

Are employers required to cover GLP-1 drugs for weight loss?

Generally, employers are not legally required to cover GLP-1 drugs for weight loss. Coverage decisions are typically based on the terms of the employer’s health insurance plan and their assessment of the cost-benefit ratio.

-

What types of coverage restrictions are employers implementing?

Employers are implementing various restrictions, including requiring a specific BMI, mandating participation in weight management programs, obtaining prior authorization, increasing cost-sharing, and limiting the duration of coverage.

-

How will these coverage changes impact employees seeking weight loss treatment?

These changes may make it more difficult or expensive for employees to access GLP-1 drugs for weight loss. Some employees may be ineligible for coverage altogether, while others may face higher out-of-pocket costs.

-

What is the long-term outlook for employer-sponsored GLP-1 drug coverage?

The long-term outlook is uncertain. As the cost of these drugs continues to rise, employers will likely continue to explore ways to manage costs. The development of more affordable alternatives or the emergence of new research findings could also influence coverage decisions.

The evolving landscape of GLP-1 drug coverage highlights the complex interplay between healthcare costs, employee benefits, and the pursuit of improved health outcomes. As employers navigate these challenges, it’s crucial to prioritize transparency, equity, and a commitment to providing employees with access to the care they need.

What steps do you think employers should take to ensure equitable access to these medications? How can the healthcare system address the high cost of innovative drugs like GLP-1 agonists?

Discover more from Archyworldys

Subscribe to get the latest posts sent to your email.