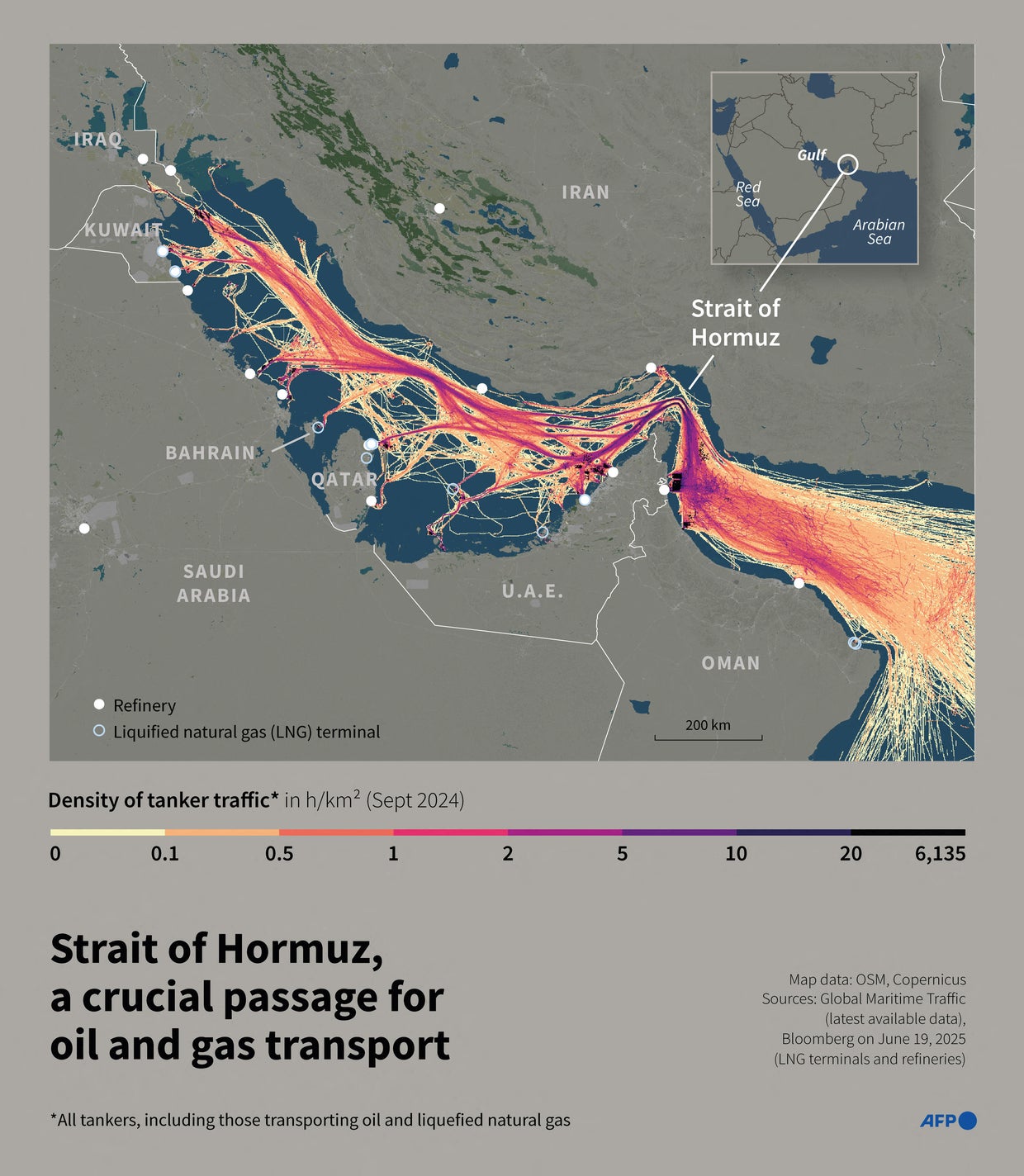

A staggering 20% of the world’s oil supply passes through the Strait of Hormuz. Now, escalating tensions and recent incidents are translating into concrete supply chain shocks for Asia’s petrochemical industry, with force majeure declarations rapidly multiplying. This isn’t a temporary blip; it’s a harbinger of a new era where feedstock risk eclipses demand-side concerns as the primary driver of market volatility.

The Domino Effect of Hormuz Disruptions

The initial reports – Aster (Singapore) halting raw material supplies, Wanhua (China) invoking force majeure on Middle East deliveries, and Korean petrochemical makers facing deepening crises – were alarming enough. However, these are likely just the first waves. ICIS reports a “very grim” outlook, predicting further force majeure notices across the region, particularly in Singapore. The Economic Development Board (EDB) of Singapore is actively engaging with industry players, a clear indication of the severity of the situation.

Beyond Immediate Supply Shocks: A Paradigm Shift

Historically, Asian petrochemical markets have largely focused on managing demand fluctuations and optimizing production capacity. While these factors remain important, the current crisis underscores a critical vulnerability: over-reliance on a single, geographically concentrated supply route for essential feedstocks. This isn’t simply about price increases; it’s about the potential for complete production halts, jeopardizing downstream industries and impacting global supply chains.

The Rise of Regionalization and Diversification

The immediate response to feedstock disruptions is, predictably, price speculation and attempts to secure alternative supplies. However, the long-term implications point towards a fundamental restructuring of supply chains. We can expect to see:

- Increased Regionalization: Companies will prioritize sourcing feedstocks from within Asia, even if it means higher costs, to reduce geopolitical risk.

- Diversification of Supply Routes: Exploration of alternative shipping lanes and investment in infrastructure to bypass the Strait of Hormuz will accelerate.

- Strategic Stockpiling: Governments and companies will likely build up strategic reserves of key feedstocks to buffer against future disruptions.

- Investment in Alternative Feedstocks: Greater focus on developing and utilizing alternative feedstocks, such as bio-based materials and recycled plastics, to reduce dependence on traditional oil-based sources.

The Impact on C2 Markets and Beyond

The C2 (ethylene) market, heavily reliant on naphtha sourced from the Middle East, is at the epicenter of this crisis. However, the ripple effects will extend to all petrochemical derivatives, impacting industries from packaging and automotive to construction and healthcare. Companies that proactively address feedstock risk will be best positioned to weather the storm and capitalize on emerging opportunities.

Consider the potential for increased investment in ethane cracking facilities in regions with access to shale gas resources. While this requires significant capital expenditure, it offers a pathway to greater feedstock independence and long-term cost competitiveness.

| Feedstock | Current Reliance on Hormuz Route | Projected Reliance (2030) – Conservative Estimate |

|---|---|---|

| Naphtha | 75% | 50% |

| Ethane | 20% | 30% |

| Propane | 60% | 40% |

Navigating the New Normal: A Proactive Approach

The disruptions in the Strait of Hormuz are not an isolated incident. They are a symptom of a broader trend towards increased geopolitical instability and supply chain vulnerability. Companies must move beyond reactive crisis management and adopt a proactive, risk-based approach to feedstock sourcing. This includes conducting thorough supply chain risk assessments, developing contingency plans, and investing in diversification and resilience.

The future of Asia’s petrochemical industry hinges on its ability to adapt to this new reality. Those who embrace change and prioritize feedstock security will thrive, while those who remain complacent risk being left behind.

Frequently Asked Questions About Feedstock Risk

What is the biggest long-term risk facing the Asian petrochemical industry?

The biggest long-term risk is the continued vulnerability of supply chains to geopolitical disruptions, particularly in key chokepoints like the Strait of Hormuz. Diversification and regionalization are crucial mitigation strategies.

How will these disruptions impact petrochemical prices?

Expect continued price volatility in the short to medium term. Longer-term, prices will likely stabilize at a higher baseline as companies factor in the cost of increased feedstock security.

What role will alternative feedstocks play in mitigating risk?

Alternative feedstocks, such as bio-based materials and recycled plastics, will become increasingly important as companies seek to reduce their reliance on traditional oil-based sources. However, scaling up production of these alternatives will require significant investment and technological advancements.

What are your predictions for the future of feedstock security in Asia? Share your insights in the comments below!

Related reading

Discover more from Archyworldys

Subscribe to get the latest posts sent to your email.